No one will deny the preciousness and value of life.

Life Insurance

Life, which is the most basic and fundamental value of life, cannot be artificially controlled.

But at least buying life insurance can protect your loved ones and property.

So, what is life insurance and why should you sign up for it?

- Funeral expense

- To cover children’s expenses

- Replace the spouses’ income

- Mortgage, Debt and to pay off debt

- To buy a business partner’s shares

- Pay off estate taxes

If you wish to learn more, please contact us by filling the estimate form.

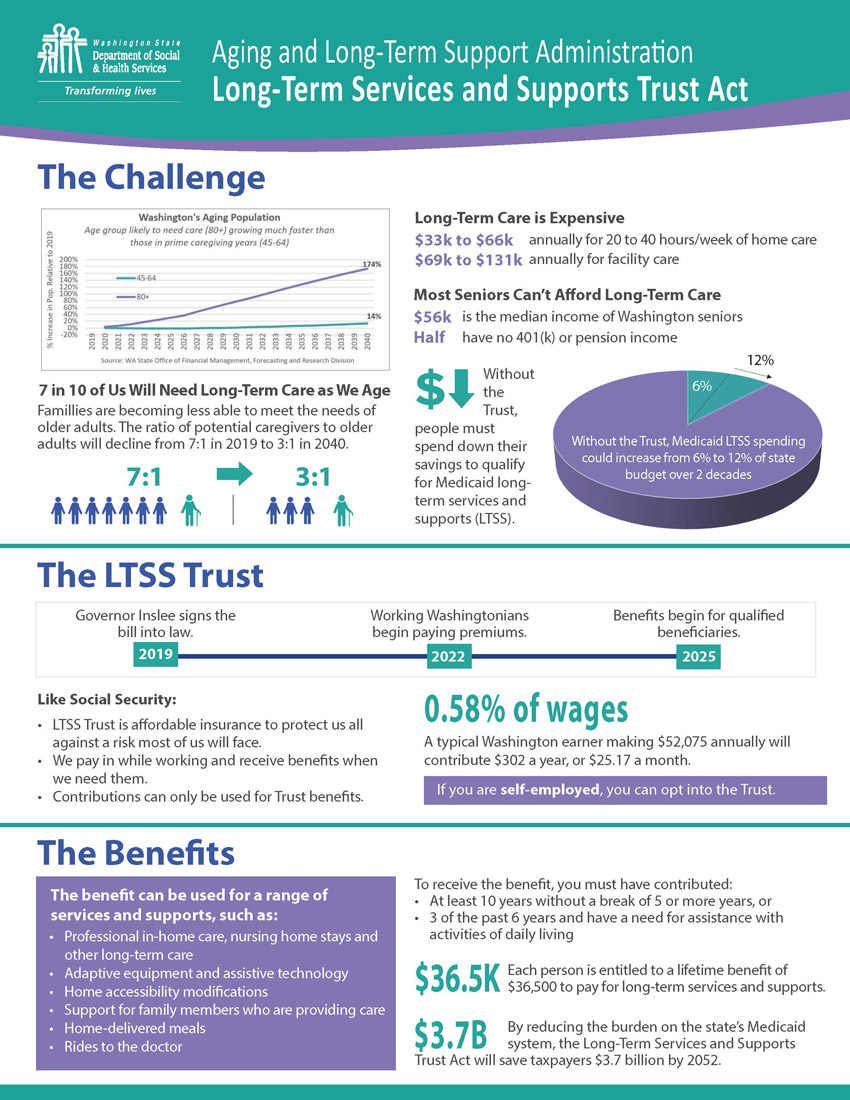

New State of Washington Long Term Care Act

Washington State will pass a new tax law on employees in 2019 to fund publicly operated long-term care (LTC) insurance programs, and effective January 1, 2022, Washington residents who are W-2 employees will be able to pay their salaries for this program. Enforces a payroll tax collection of 0.58%.

For example, you would pay an additional tax of $580 per $100,000 reward.

You must purchase the LTC policy by 11/01/2021 to be exempt from taxes and programs.

What is long-term care insurance?

LTC is a disability judgment when two or more of the six normal activities are impossible due to illness or old age.

If you use a caregiver or nursing facility or nursing facility in these circumstances, we will provide a fee to cover some or all the cost of those services. This cost is very expensive, and the aging population is rapidly progressing, so it is difficult for anyone except those who receive Medicaid to prepare for it.

What are the 6 normal activities?

Eating, going to the bathroom, washing, taking medicine, getting dressed, managing finances.

Why do you run this program by collecting taxes?

In fact, when Obamacare launched in 2013, they tried to force this LTC benefit into place. The cost of this was too high to implement.

Like most states, Washington has an aging population. And the cost of caregivers and nursing homes in old age is extremely high. This is an individual problem, but it is also a serious social problem.

With this tax levy now starting in 2022, Washington State is attempting to alleviate some of this problem. In other words, we see this phenomenon as a social crisis and try to solve it through policy.

What are the benefits of LTC in this new law?

Taxpayers who have paid their taxes over a period can receive up to $100 per day to cover their LTC costs in the event of a disability, with a maximum, lifetime benefit of $36,500. Long-term care costs up to $100, equivalent to one year’s coverage.

- Benefit of $100 per day, $36,500 for lifetime

- Typically used for caregiver, Adult Daycare, and Nursing home expenses.

- Benefits are not available outside of Washington State. Available only in Washington.

- Applies only to taxpayers who pay this tax.

- If only one of the married couples receives a monthly salary, only the person receiving the salary is required to pay. However, only the payer will receive the cover.

What do I need to do to receive the benefits?

To qualify for the benefit, you must pay the tax for 10 years and at least 3 to 5 years in a row. Otherwise, you will not see any benefits.

Who is subject to this new tax?

Effective January 1, 2022, a new payroll tax will be compulsory for all W-2 employees. This tax is compulsory by the employer and paid by the employee through payroll withholding. (In other words, the actual wage will decrease.)

This tax does not apply to self-employed individuals who do not receive a W-2 but may choose to participate in the program.

How much tax do I pay?

There is a payroll tax of 0.58% of your gross salary.

Gross salary has no income limit and includes regular salaries, bonuses, and company stock.

For example:

An employee with an annual income of $100,000 pays an LTC tax of $580 per year.

An employee in the IT industry with an annual remuneration of $160,000 ($160,000 salary + $290,000 Best RSU (stock option)).

You pay an extra $2,610 in payroll tax.

How can I get a waiver of this new payroll tax?

If you have an LTC product that offers the same or better benefits before November 1st, you may be able to waive this tax.

Eligible products are LTC, life insurance with LTC coverage, and annuity products with LTC coverage are exempt from this tax, which must be at least the coverage provided by this new law.

However, benefits included in life insurance as a chronic illness rider are not recognized. It must be a qualified LTC benefit to qualify for a waiver.

What is the difference between a state plan and private LTC insurance?

Individually enrolled plans vary in coverage. (Content, Coverage Period, Coverage Amount)

State plans have no inflation protection at all, while private plans have.

Part or all your premium may be tax deductible. (Tax deduction is determined by age)

Individual long-term care insurance covers a minimum of two years.

Couples can receive a discount if they sign up together.

It can be used anywhere in the United States other than Washington.

Cash pickup is also possible.

Would it be better to buy personal LTC insurance or buy a state plan?

We recommend that you prepare a personal alternative plan for people who:

- Those who think the compensation of $100 per day and $3,000 per month is too small.

- High Income: means a person who earns $300,000 or more in annual employee remuneration. Most can find much better long-term insurance alternatives for far less than $1,740 per year ($300,000 * 0.58% payroll tax).

- Plan to move out of state after retirement: You can only get these benefits if you are receiving treatment in Washington State.

- However, you must pay this tax for at least three to five consecutive years to be eligible for benefits. Otherwise, you will not see any benefits.

- Those who want to take advantage of tax benefits.

The state will cover part of the cost through social awareness of the need for LTC benefits, institutional treatment, and taxes. However, considering inflation in the future, 5, 10, 20 years from now, it is too poor.

Families 55 years of age and older and under $50,000 are encouraged to use the state plan. It is good to have a meager but low-cost benefit. However, young people and high-income people are advised to compare individual plans and state plans. You can get a better plan for the same cost.

ACE Insurance and Retirement Services Inc.

Danny Kim

425-890-1260